What Should You Know About Surplus Distribution

Hereطs a piece of good news you probably didn’t expect: if you’ve bought comprehensive or third party car insurance in Saudi Arabia before, your insurance company might actually owe you money. Yes, really! It’s all thanks to something called surplus distribution.

Not sure what surplus means or how to check your surplus eligibility? Don’t worry—this guide breaks it down for you & shows how surplus distribution might help you get low price car insurance Saudi Arabia.

What does Surplus mean in Insurance?

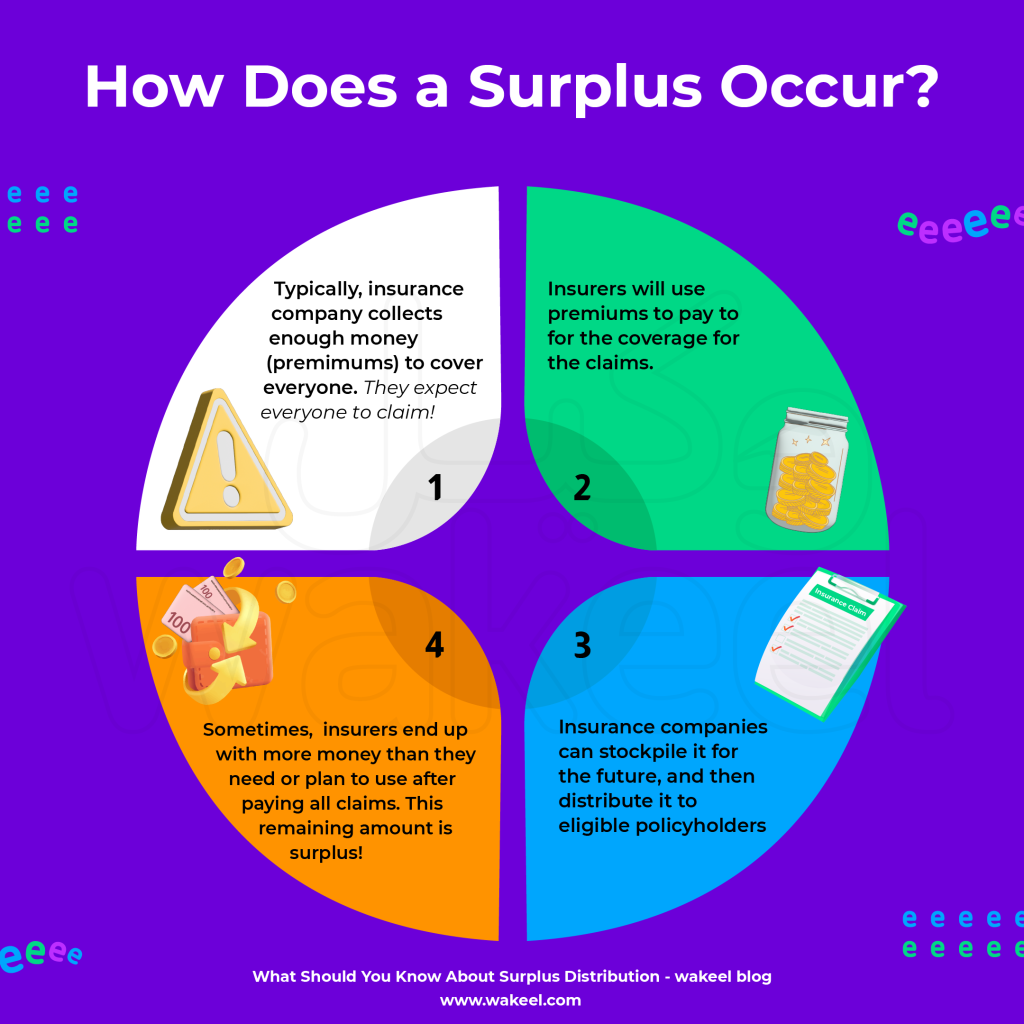

In simple terms, a surplus is what’s left when an insurance company collects more money than it spends on paying claims and running the company.

Let’s say your insurance provider collects SAR 10 million from each car owner in a year, but only needs to pay SAR 5 million to pay for accident claims. That SAR 5 million difference? That’s the insurance surplus — the money that remains after taking care of all claims and operating expenses.

So, where does all that extra money come from?

Car insurance in Saudi Arabia works under the cooperative insurance model, known as takaful. In this model, the money you pay for your car insurance isn’t treated as company profit! Instead, it’s held in trust.

Saudi insurance companies use the money they collect from customers to pay claims and cover operating costs. If there’s money left over at the end of the year, that surplus doesn’t stay with the company—it must go back to the eligible customers.

The Saudi Insurance Authority requires insurance companies to share at least 10% of their surplus with their customers. To be eligible, you need to:

- Keep your insurance active. Don’t cancel it early! If you cancel your insurance to sell your car or transfer vehicle ownership, then you won’t be eligible.

- Avoid making too many claims. Your claims shouldn’t cost the company more than 70% of what you paid for your car insurance.

- Be debt-free: You can’t owe the insurance company any money.

Use Najm to check how much surplus you’re entitled to 💰

Just check the Najm app or website. You can check your surplus balance from previous years too.

Najm Surplus Service

- You can also check Tawuniya surplus eligibility directly on their app or website.

- Same for Al Rajhi, check your surplus eligibility directly on their app or website.

How much money do you get from the surplus?

Let’s set expectations: insurance surplus amount is usually quite small—often no more than 4 riyals. That said, it’s still your money, and you have a say in how it’s used. You can choose to:

- Get it transferred: You can simply ask the company to credit the money directly into your bank account.

- Use it as a discount: You can keep it and use it as a discount when your renew car insurance

- Donate it to charity: Give the company your permission to donate the surplus on your behalf to a good cause.

Small as it may be, but it’s always nice to get some money back from your insurance!

Bottom line?

You won’t get rich from this. But surplus distribution is a good sign that the company is managing risks well and sharing profits with customers

So, the next time you compare car insurance prices in Saudi — give an advantage to the companies that have been able to distribute surplus in recent years.